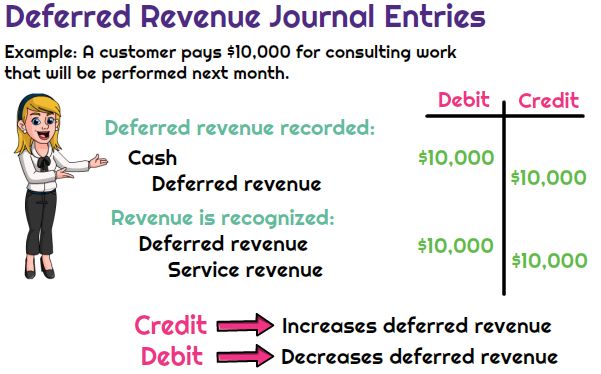

Deferred revenue, also known as “unearned revenue”, is a term that’s used to describe payments that a business has received in advance for goods or services that haven’t yet been delivered but should be in the future.

Deferred revenue should be recorded and treated as a liability rather than an asset or actual revenue because it reflects revenue that hasn’t yet been earned; delivery of the product or service to the customer is still outstanding.

For argument’s sake, let’s say that a customer makes an advance payment of $1,200 for 12 months’ use of a service. Although the $1,200 appears in the business’s bank account immediately, it can only be recognized as revenue proportionally over the 12-month period (i.e., $100 per month) because the service is provided on a monthly basis.

Keep in mind that if the service is not delivered as planned (e.g., because the customer cancels their subscription) part of the monies already paid may be owed back to the customer.

Deferred Revenue Explained:

FAQs

Visibility over deferred revenue helps brands accurately account for income over time, especially for subscription-based or long-term service contracts.

Deferred revenue is income for goods or services not yet provided, while accrued revenue is income for services rendered but not yet paid for. The key difference between deferred and accrued revenue is that deferred revenue is a liability.

Deferred revenue is income that has been received by a company but has not yet been earned. It represents an obligation to deliver goods or services in the future.